[ad_1]

Month-to-month development output is estimated to have elevated 0.4% in quantity phrases in September 2023, in response to the ONS.

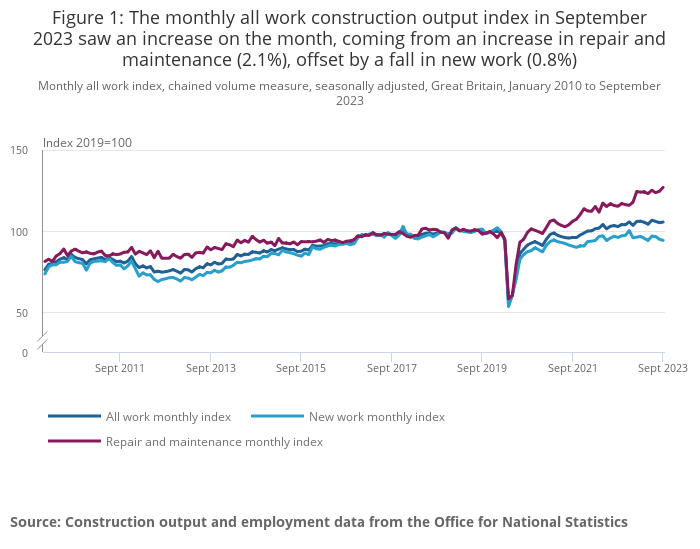

This got here solely from a 2.1% improve in restore & upkeep between August and September as new work slowed by 0.8%.

Anecdotal proof obtained from survey returns the nice and cozy, dry climate in September helped promote development exercise. Based on the Met Workplace, September 2023 was the joint hottest September on file for England and Wales.

Non-public housing restore & upkeep was the quickest rising subsector, rising by 3.0%. Britain, it appears, was actually fixing its roofs whereas the solar shone.

Throughout the third quarter of the 12 months, July to September, development output elevated by 0.1% in contrast with the second quarter, because of a 0.7% rise in restore & upkeep; new work noticed a lower of 0.3%.

Whereas third quarter development was even weaker than Q2’s development of 0.3%, the numbers are nonetheless in optimistic territory, indicating that the British development trade just isn’t in recession.

Throughout the economic system as an entire, gross domestioc product (GDP) flatlined within the third quarter, exhibiting no change fromt eh second quarter (0.0% development).

Whole development new orders in Q3 elevated by 3.9% (or £393m) over Q2. This quarterly rise in orders got here primarily from public different new orders and infrastructure new orders, which elevated 23.7% (£265m) and 14.3% (204m) respectively.

The annual fee of development output worth development was 3.9% within the 12 months to September 2023. This has slowed from the file annual worth development in Might 2022, when it hit 10.4%.

Clive Docwra, managing director of property and development consultancy McBains, stated: “Immediately’s figures will present a measure of aid for the development trade, coming off the again of two successive months of falling output.

“Whereas we’ve got seen a small uptick in improvement lending, the place schemes that have been beforehand unviable have been re-purposed to align with present market situations, this isn’t reflective of total market sentiment, as evidenced by immediately’s figures exhibiting a 0.8% lower in new work on the earlier month.

“Our purchasers inform us that borrowing prices are nonetheless deterring some investments, and whereas rates of interest might have peaked, the longer-term outlook stays unsure.

“On the plus facet, the trade will welcome complete development orders rising over the third quarter of 2023 in contrast with the earlier quarter, on account of new work within the public and infrastructure sectors, however quantity housebuilding will take extra time to see a turnaround whereas rates of interest stay excessive.”

Fraser Johns, finance director at Beard stated: “Following the PMI knowledge earlier this week which confirmed a decline in output in October, information this morning of a 0.4% uplift in quantity in September reveals simply how unpredictable and unstable the sector is within the present local weather. Though the month noticed a fall in new work, when considered within the context of the quarter, there was truly a 3.9% rise in comparison with Q2 2023.

“The most important contributors to this rise was infrastructure new orders (14.3%) and non-housing public new work (23.7%), significantly for faculties and faculties. This definitely displays our personal experiences at Beard as each regional and nationwide frameworks proceed to be an excellent supply of labor and a driver in pipeline exercise. The schooling sector stays a buoyant marketplace for Beard with begins on web site throughout main, secondary and additional schooling in current months. Information of a rise in new housing orders will definitely be encouraging for these contractors reliant on the housing market, though the sector nonetheless faces actual challenges in a sustained greater curiosity atmosphere.

“September’s uplift and the marginal quarter-to-quarter development was brought about predominantly by an increase in restore & upkeep, demonstrating that the urge for food or capacity to decide to new constructing tasks remains to be clearly dampened. Because of this, the message stays the identical; we should stay open and clear in our conversations with purchasers and stakeholders, all whereas doing what we will to minimise strain on value plans.”

Bought a narrative? E-mail information@theconstructionindex.co.uk

[ad_2]